The retail method of valuing inventory only provides an approximation of inventory value since some items in a retail store will most likely have been shoplifted, broken, or misplaced. It’s important for retail stores to perform a physical inventory valuation periodically to ensure the accuracy of inventory estimates as a way to support the retail method of valuing inventory. Doing so can save you time at the end of the year when you’re preparing tax statements, and it helps you keep track of your revenue and profits. The LIFO (Last In, First Out) accounting method considers the last items purchased as the first ones sold, making it the opposite of the FIFO (First In, First Out) method. Therefore, the cost of sales is determined by the price of items purchased most recently.

Ways to Account for Inventory Costs in Retail Accounting

- During reconciliation, if any discrepancies, errors, or unauthorized expenses are found, you should make the appropriate adjustments and mark them in your general ledger.

- Even offering discounts on certain products would throw off your calculations.

- The advantage of this is that COGS at retail is just sales and is much easier to track than actual COGS.

- This way, retailers greatly simplify the way they track items, saving loads of valuable time in the process.

- During the quarter, your sales recorded through our point of sale system reached $40,000.

If you can’t keep track of every item on hand, you must make an assumption about which ones you sell first to calculate the cost of your inventory. Whichever you sell first is unknowable, but the assumption keeps your books consistent. Since the retail inventory method is just an estimation technique, expect that there will be differences in the physical count and retail method estimations. In this case, 15 of the 50 dice you’ve sold would have cost 10 cents ($1.50), 25 of the dice cost 7 cents ($1.75), and 10 dice cost 5 cents ($0.50).

Demystifying Retail Accounting: A Guide for Business Growth

It limits your ability to price your products dynamically and strategically to compete in the marketplace. You could miss out on raising the price of one item because you don’t want to increase the prices of others. Of course, using the retail method, for this reason, has a problematic implication. Namely, using a flat markup rate for all your company’s products usually isn’t a good idea. In addition, few businesses legitimately sell their what is retail accounting most recently acquired units first.

Retail inventory method

This retail accounting strategy will be the best option for start-up organizations, offering a new approach to inventory management and cost estimation. More specifically, in retail accounting, you’ve got to value all of your inventory at retail value and then subtract your sales to estimate your remaining inventory. This will also help you determine the markup on your items, which can be used to calculate how much inventory you have left after the sale. In other words, retail accounting is a way of tracking inventory costs that is especially simplified compared to the other available methods.

When To Use The Retail Method & Who Is It Best For

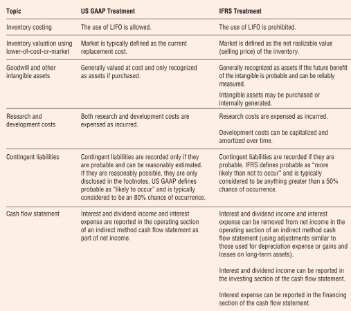

Of course, this gets more complicated when there is more than one type of item with different prices. The pricing, price changes, and price change rates for all units of a single item are the same. You also make the assumption that all units of the same item will have the exact pricing, price changes, and price change rates. HashMicro is Singapore’s ERP solution provider with the most complete software suite for various industries, customizable to unique needs of any business. However, the specific method of calculating the value of ending inventory (e.g., FIFO, LIFO) can affect your COGS and, consequently, your reported profits.

What Is Retail Accounting? Retail Method + Calculator

But knowledge without application is like a compass without a map – it might point you in the right direction, but it won’t help you navigate the journey. This section is your action guide, transforming theoretical knowledge into practical tools for managing your retail business effectively. Strong financial management, fueled by a solid understanding of retail accounting, is the key to unlocking the full potential of your business. Because there’s no guarantee you’ll be able to change your accounting methods https://www.instagram.com/bookstime_inc later, you must choose them carefully the first time.

What does an accountant do in a retail store?

Cost accounting for retail tracks each item based on the total cost paid for purchased inventory. A retail business owner has to understand that the numbers these https://www.bookstime.com/ methods provide will not be as accurate as a physical inventory count, but they will save time. Retail accounting is a specific method of accounting that assists companies in tracking inventory without manually counting all of the items in the store or warehouse. Retail method is an inventory management technique that helps estimate the value of inventory based on the retail prices of their goods rather than the cost price. This method makes it easier for retailers to manage extensive inventories without diving deep into complex calculations.

- The primary reason retail accounting is different from accounting in other industries is that retail stores must keep track of their inventories.

- You could miss out on raising the price of one item because you don’t want to increase the prices of others.

- Barcode scanning is beneficial during busy periods, such as sales events, when keeping track of stock is crucial.

- The central point of this method is estimating the retailer’s ending inventory balances.

- The operational dashboard gives you real-time visibility of all stock activities, allowing you to make informed decisions quickly.

- Then to find the ending inventory, you’ll multiply your sales by the cost-to-retail percentage, then subtract it from your beginning inventory.

Weighted average method of accounting

The balance sheet presents your assets, liabilities, and equity, while the cash flow statement tracks the movement of cash in and out of your business. FIFO, which stands for “First-In, First-Out,” is a retail accounting method based on the assumption that the oldest items in your inventory are the first to be sold. This method is frequently employed by retail businesses dealing with time-sensitive products, like trendy fashion items or perishable goods typically found in convenience stores. Retail accounting software can provide a comprehensive account inventory at the item’s retail price in order to detect losses, damages and theft of stock.

Accrual accounting and tax rules for companies with inventories are complex, and you shouldn’t try to navigate them alone. Unfortunately, inventory accounting is essential for creating accurate financial statements and reports. In most cases, it’s simultaneously your business’s most significant asset and expense. He has a CPA license in the Philippines and a BS in Accountancy graduate at Silliman University. Use the calculator below to compute your estimated ending inventory at cost using the conventional or average method of retail accounting. If, for example, a game store employee accidentally breaks a collector’s figurine or items are stolen, the POS system can’t account for the loss.